Most people have heard of fracking in the context of oil and gas (O&G) drilling and maybe a few of them know that this can be done in horizontal drilling at a distance from the surface well hole. Explosives or hydraulic pressure is used to fracture a section of rock formation surround the drill hole and then frac sand is forced into the fractures to prop them open. Sometimes the sand is referred to as a proppant. This increases the permeability of the formation and, hopefully, increases the productivity of the well.

The first directional drilling was performed in 1930 from shore at Huntington Beach, CA, into an offshore deposit of oilsands.

The fracking controversy stems from evidence that fracturing can lead to O&G migration into ground water and then into drinking water. This essay does not address this matter.

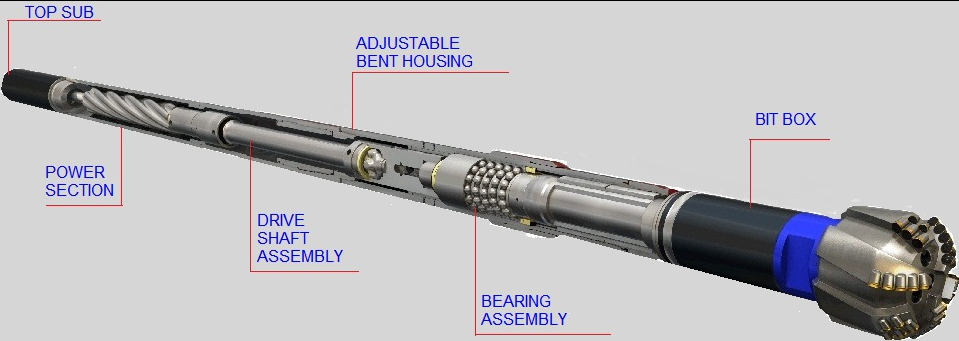

Within the O&G drilling world is the question of how far laterally a hole can be drilled and to what extent it pays. According to one source, in 1997 the lateral distance stood at about 500 ft to completion. At present it stands at 3 miles with 4 miles becoming more common. Greater length requires an upgrade in drilling equipment to handle the extra power demands.

Today there are steerable down-hole mud motors that can rotate the drill bit independent of the drill string. Mud is pumped downhole at high pressure to rotate a rotor connected to the bit. The rotor fits in a stator near the end of the drill string. A steerable feature is able to bend ~3 to 4 degrees.

In the literature there is mention of the issues in vertical drilling through a steeply inclined fault. As the bit penetrates a steep fault surface it could slip and lead to damage of the drill string and casing. Better to penetrate a fault perpendicular to the fault plane with directional drilling.

There are many good reasons for a driller to use directional drilling.

A borehole that has gone off-course can be redirected to the desired direction from the same borehole.

From a single drilling site multiple boreholes can be drilled, each going to a different part of the formation.

During a well blow-out or fire, a new borehole can be drilled from a distance to intercept the blown-out borehole and pump material into it to control the blow-out.

A drilling site can be situated away from a settlement or body of water and still get to the oil reservoir by directional drilling.

Directional drilling can be performed in an existing well where equipment or debris is blocking the original bore hole.

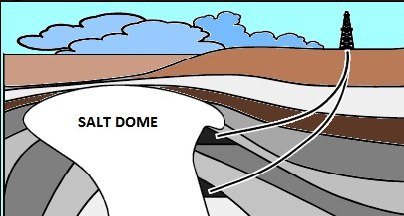

Drilling through a salt dome is problematic for several reasons. A soft formation like a salt dome can result in bit balling where the tricone bit packs with debris and the wheels quit turning. Wellbore erosion, salt creep, and excessive mud losses can occur as well.

Salt domes form from plastic deformation of an underlying low density and ductile salt layer (90 to 99 % halite) into a fault or fracture where it is subject to movement by lateral forces of the surrounding sediment layers. These lateral forces push the salt formation in the direction of weakest forces which is generally upwards. Irregular features in the salt dome can lead to collection of oil and gas pockets. Lateral drilling can be used to access the reservoirs, bypassing the salt formation.

Wow. A study was published calculating the number of living cells currently present on Earth and the number that have ever lived. The paper, titled “The geologic history of primary productivity,” was published in Current Biology, October 11, 2023. Sadly, the full article rests behind a paywall. But the abstract is open access so I will reproduce it here.

The lead author, Peter Crockford, is a geologist at Carleton University.

Abstract: The rate of primary productivity is a keystone variable in driving biogeochemical cycles today and has been throughout Earth’s past. 1 For example, it plays a critical role in determining nutrient stoichiometry in the oceans,2 the amount of global biomass,3 and the composition of Earth’s atmosphere.4 Modern estimates suggest that terrestrial and marine realms contribute near-equal amounts to global gross primary productivity (GPP).5 However, this productivity balance has shifted significantly in both recent times 6 and through deep time.7,8 Combining the marine and terrestrial components, modern GPP fixes ≈250 billion tonnes of carbon per year (Gt C year−1).5,9,10,11 A grand challenge in the study of the history of life on Earth has been to constrain the trajectory that connects present-day productivity to the origin of life. Here, we address this gap by piecing together estimates of primary productivity from the origin of life to the present day. We estimate that ∼1011–1012 Gt C has cumulatively been fixed through GPP (≈100 times greater than Earth’s entire carbon stock). We further estimate that 1039–1040 cells have occupied the Earth to date, that more autotrophs than heterotrophs have ever existed, and that cyanobacteria likely account for a larger proportion than any other group in terms of the number of cells. We discuss implications for evolutionary trajectories and highlight the early Proterozoic, which encompasses the Great Oxidation Event (GOE), as the time where most uncertainty exists regarding the quantitative census presented here.

An article by Elizabeth Pennisi was published in Science which is a decent summary of the paper. The Science review reports that the number of cells alive today amounts to 1030 cells with most of them cyanobacteria. The total number of cells to ever have lived is estimated to be between 1039 and 1040. The article goes further and says that the resources on Earth cannot support more than 1041 cells.

While cockeyed optimists are working toward a new age of electric vehicles in the glare of an admiring public, I find myself standing off to the side mired in skepticism. What are the long-term consequences of large-scale electrification of transportation?

The industrial revolution as we in the west see it began as early as 1760 and continues through today. Outwardly it bears some resemblance to an expanding foam. A foam consists of a large number of conjoined bubbles, each representing some economic activity in the form of a product or service. A business or product hits the market and commonly grows along a sigmoidal curve. Over time across the world the mass of growing bubbles expand collectively as the population grows and technology advances. Bubbles initiate, grow and sometimes collapse or merge as consolidation and new generations of technology come along and obsolescence takes its toll.

The generation of great wealth often builds from the initiation of a bubble. The invention of the steam engine, the Bessemer process for the production of steel, the introduction of kerosene replacing whale oil, the Haber process for the production of ammonia and explosives, and thousands of other fundamental innovations to the industrial economy played part in the growing the present mass of economic bubbles worldwide.

After years of simmering on the back burner, electric automobile demand has finally taken off with help from Tesla’s electric cars. Today, electric vehicles are part of a bubble that is still in the early days of growth. The early speculators in the field stand the best chance of winning big market share. A major contribution to this development is the recent availability of cheap, energy dense lithium-ion batteries.

Of all of the metals in the periodic table, lithium is the lightest and has the greatest standard Li+/Li reduction potential at -3.045 volts. The large electrode potential and the high specific energy capacity of Lithium (3.86 Ah/gram) makes lithium an ideal anode material. Recall from basic high school electricity that DC power = volts x amps. Higher voltage and/or higher amperage gives higher power (energy per second). Of all the metals, lithium has the highest reduction potential (volts).

Rechargeable lithium batteries have high mass and volume energy density which is a distinct advantage for powering portable devices including vehicles. Progress in the development of lithium-ion batteries was worth a Nobel Prize in 2019 for John B. Goodenough, M. Stanley Whittingham and Akira Yoshino.

All of this happy talk of a lithium-powered rechargeable future should be cause for celebration, right? New deposits of lithium are being discovered and exploited worldwide. But cobalt? Not so much. Alternatives to LiCoO2 batteries are being explored enthusiastically with some emphasis on alternatives to cobalt. But, the clock is ticking. The more infrastructure and sales being built around cobalt-containing batteries, the harder it will become for alternatives to come into use.

One of the consequences of increasing demand for lithium in the energy marketplace is the effect on the price and availability of industrial lithium chemicals. In particular, organolithium products. The chemical industry is already seeing sharp price increases for these materials. For those in the organic chemicals domain like pharmaceuticals and organic specialty chemicals, common alkyllithium products like methyllithium and butyllithium are driven by lithium prices and are already seeing steep price increases.

Is it just background inflation or is burgeoning lithium demand driving it? Both I’d say. Potentially worse is the effect on manufacturers of organolithium products. Will they stay in the organolithium business, at least in the US, or switch to energy-related products? It is my guess that there will always be suppliers for organolithium demand in chemical processing.

A concern with increasing lithium demand has to do with recycling of lithium and perhaps cobalt. Hopefully there are people working on this with an eye to scale up soon. A rechargeable battery contains a dog’s lunch of chemical substances, not all of which may be economically recoverable to specification for reuse. In general, chemical processes can be devised to recover and purify components. But, the costs of achieving the desired specification may price it out of the market. With lithium recovery, in general the lithium in a recovery process must be taken to the point where it is an actual raw material for battery use and meets the specifications. Mines often produce lithium carbonate or lithium hydroxide as their output. Li2CO3 is convenient because it precipitates from aqueous mixtures. It must also be price competitive with “virgin” lithium raw materials as well.

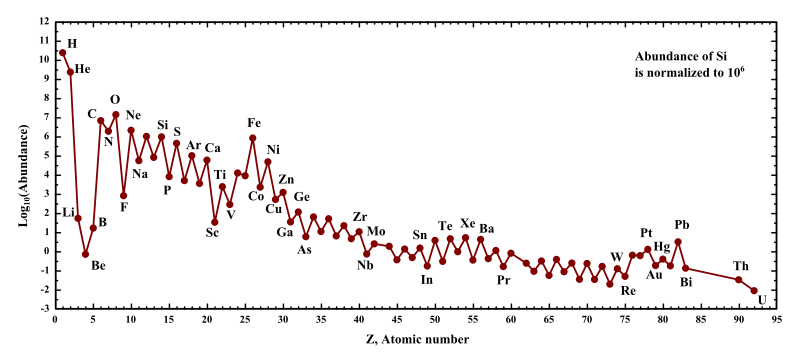

Lithium ranks 33rd in terrestrial abundance and less than that in cosmic abundance. Unlike some other elements like iron, lithium nuclei formed are rapidly destroyed in stars throughout their life cycle. Lithium nuclei are just too delicate to survive stellar interiors. The big bang is thought to have produced a small amount of primordial lithium-7. Most lithium seems to form during spallation reactions when galactic cosmic rays collide with interstellar carbon, nitrogen and oxygen (CNO) nuclei and are split apart from high energy collisions yielding lithium, beryllium and boron- LiBeB. All three elements of LiBeB are cosmically scarce as shown on the chart below.

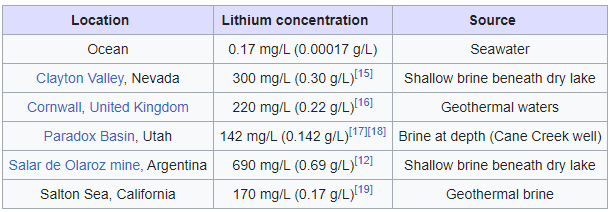

Lithium is found chiefly in two forms geologically. One is in granite pegmatite formations such as the pyroxene mineral spodumene, or lithium aluminum inosilicate, LiAl(SiO3)2. This lithium mineral is obtained through hard rock mining in a few locations globally, chiefly Australia.

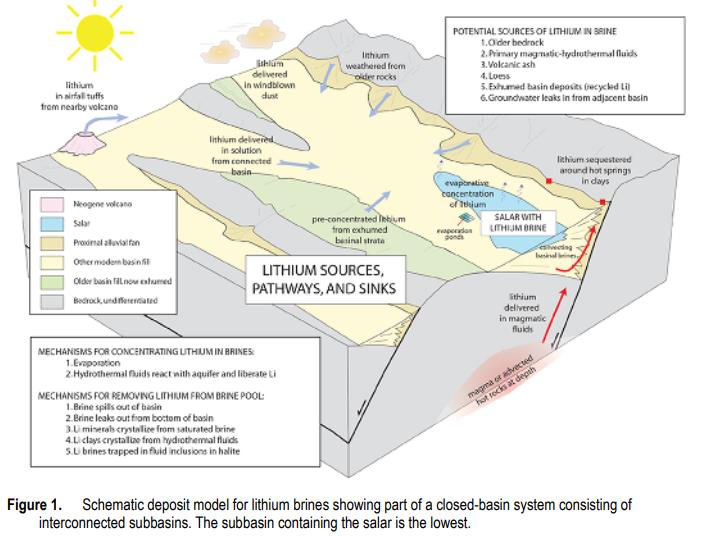

Source: “A Preliminary Deposit Model for Lithium Brines,” Dwight Bradley, LeeAnn Munk, Hillary Jochens, Scott Hynek, and Keith Labay, US Geological Survey, Open-File Report 2013–1006, https://pubs.usgs.gov/of/2013/1006/OF13-1006.pdf

Chemical Definition: Salt; an ionic compound; A salt consists of the positive ion (cation) of a base and the negative ion (anion) of an acid. The word “salt” is a large category of substances, but for maximum confusion it also refers to a specific compound, NaCl or common table salt. In this post the word refers to the category of ionic compounds.

The other source category is lithium-enriched brines. The US Geological Survey has proposed a geological model for brine or salt deposition. According to Bradley, et al.,

“All producing lithium brine deposits share a number of first-order characteristics: (1) arid climate; (2) closed basin containing a laya or salar; (3) tectonically driven subsidence; (4) associated igneous or geothermal activity; (5) suitable lithium source-rocks; 6) one or more adequate aquifers; and (7) sufficient time to concentrate a brine.”

Lithium and other soluble metal species are extracted from underground source rock by hot, high pressure hydrothermal fluids and eventually end up in subsurface, in underwater brine pools or on the surface as a salt lake or a salt flat or salar. These deposits commonly accumulate in isolated locations that have prevented drainage. An excellent summary of salt deposits can be found here.

Critical to any kind of mineral mining is the definition of an economic deposit. The size of an economic deposit varies with the market value of the mineral, meaning that as the value per ton of ore increases, the extent of the economic deposit may increase to include less concentrated ore. If you want to invest in a mine, it is good to understand this. A good opportunity may vanish if the market price of the mineral or metal drops below the profit objectives. Hopefully this happens before investment dollars are spent digging dirt.

Lithium mining seems to be a reasonably safe investment given the anticipated demand growth unless страшный товарищ путины invasion of Ukraine lets the nuclear genie out of the bottle.

Just for fun, there is an old joke about the definition of a mine-

Mine; noun, a hole in the ground with a liar standing at the top.

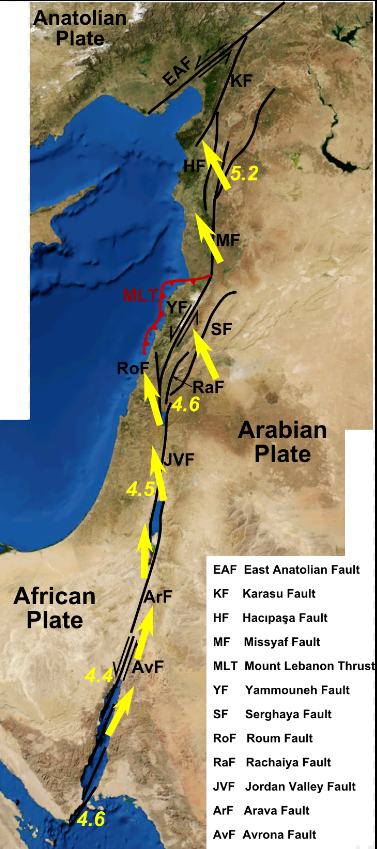

The US Geological Survey (USGS) has technical information on the Feb.6, 2023, magnitude 7.8 earthquake in southern Turkey. The event happened at 1:17:35 UTC and the epicenter located at 37.174°N 37.032°E at 17.9 km depth. The strike slip quake occurred in a seismically active region near the triple-junction of the Anatolia, Arabia, and Africa plates. As of this writing the exact location isn’t clear but the USGS suspects it happened either along the Eastern Anatolian Fault zone or the Dead Sea transform fault zone.

According to USGS, the East Anatolian fault accommodates the westward motion of Turkey towards the Aegean Sea and the Dead Sea Transform accommodates the northward motion of the Arabian plate.

The quake was reportedly felt as far away as Istanbul, Tbilisi and Cairo.

Some years back I visited the large CC&V open pit gold mine by Cripple Creek, Colorado. Standing at the bottom of the pit we could see haul trucks busily transferring ore to a staging site. Suspecting that it might be overburden, I asked what they were doing. Our guide, a geologist, said that this ore would be staged as unrefined until the price of gold rose to a certain higher value. The whole ore body had been mapped 3-dimensionally so at any given location and level where they blast, they have a rough idea of how much gold is present. At the time, ~10 years back, the geologist said that each large haul truck was typically carrying about $10,000 worth of gold. I don’t know how accurate that is, but there you have it.

The Cripple Creek gold load was discovered about 1893 and occurs in the throat of an extinct volcano. The ore contains gold and calaverite, AuTe2, a gold telluride mineral. The gold and AuTe2 is so finely dispersed that most people who work at the mine have never actually seen the gold. The recovery method they use is cyanide extraction. Unfortunately, tellurium interferes with this extraction process and unavoidably some of the gold as the telluride is left in the tailings. The ore is said to contain about 1 gram of recoverable gold per ton.

What prompted this essay was a moment of clarity I had reading a notice from the Energy Information Administration, EIA. It is common to hear about oil reserves. One might suppose that this refers to the total proven reserves in the ground. But this article referred to “economically recoverable oil resources”. When oil reserves are expressed in this way, the recoverable oil then becomes a function of the current oil prices. If oil prices are low, then the reserves are considered smaller than when oil prices are high. It seems so obvious but I never gave it a thought before. As with gold, the lesson is to pay attention to the type of reserves being discussed.

Antimony, Sb, is an obscure metalloid that rarely gets much notice outside of a few highly specialized areas of technology. The element is most often found in the mineral Stibnite, Sb2S3. Antimony is a pnictogen found in Group 5 between arsenic and bismuth in the p-block of the periodic table. Crustal abundance is 0.2 to 0.5 ppm according to Wikipedia, making it several times more abundant than silver. It has many interesting properties and uses which will be left to the reader to discover. Interestingly, there is a rare allotrope of antimony that is explosive when scratched. Luckily, this is unusual.

In a May 6, 2021, article in Forbes, writer David Blackmon cites the many uses of antimony and where it occurs in greatest natural abundance. As it turns out, the US is not one of those locations where it is found in great abundance. China has the largest abundance of antimony- greater than half of the known reserves in the world, with Russia coming in second. At present, the US imports 100 % of this key strategic material. Blackmon writes-

“Antimony is a strategic critical mineral that is used in all manner of military applications, including the manufacture of armor piercing bullets, night vision goggles, infrared sensors, precision optics, laser sighting, explosive formulations, hardened lead for bullets and shrapnel, ammunition primers, tracer ammunition, nuclear weapons and production, tritium production, flares, military clothing, and communication equipment. It is the key element in the creation of tungsten steel and the hardening of lead bullets, two of its most crucial applications during WWII.“

According to Blackmon, China currently supplies 80 % of the world’s antimony and also imports ore from other nations for refining. Here is the kicker- China may soon run short of the element. Running short of antimony doesn’t just mean that prices will rise in short supply. It could also mean that China may stop exporting much of its refined antimony in favor of internal consumption to produce goods up the value chain. China tried to do this with rare earth elements already. A country rich in strategic minerals and a sophisticated manufacturing base is a country that can wield significant power over the rest of the world. In the US, antimony is considered critical to economic and national security.

The US has had only one mining district that produced significant antimony. That would be the Stibnite mine in the Stibnite Mining District near Yellow Pine, Idaho. Mining activity stopped in the mid-1990s. The district, like most of Idaho, sits atop the granite Idaho Batholith. Volcanic activity in the past forced hot water through cracks and fissures in the rock, dissolving soluble minerals, moving mineral rich hydrothermal fluids that, when cooled, precipitated as mineral veins in the granite. Antimony minerals are often associated with another Group 5 element, arsenic, in the form of minerals like realgar and orpiment.

The Stibnite mine began as a gold mine in 1938 during the Idaho gold rush. Throughout WWII, the stibnite mine produced 40 % of the antimony and tungsten needed by the US. Tungsten, or wolfram, appears as the tungstate salt with a metal cation like iron, calcium or manganese paired with a WO4 oxoanion. The hydrothermal fluid partitions minerals in a rock formation into concentrated zones through selective solubility. This process is responsible for the formation of veins in solid rock.

Oh look. I’ve driven off into the weeds again rambling on about minerals.

There is considerable handwringing over hydraulic fracturing fluids and their potential effects on “the environment”. I use quotes in ironic fashion because I see very little parsing of the issue into relevant components. The chemical insult to the environment is highly dependent on both the substances and the extent of dispersion. But I state the obvious.

There are surface effects at the drill site and there are subsurface effects. A spill on the surface is going to be relatively small due to the limited size of the available tankage on site. I drive by these sites almost daily and can see with my own eyes the scale of the project. A surface spill of materials will be limited in scope.

The subsurface effects are complex, however, and the magnitude of consequences will depend on both the extent of the fluid penetration into aquifers and the nature of the materials in the fluid. Much criticism has been dealt, rightfully I think, over the secrecy claims on the composition of these fluids. The default reply from drillers has rested on trade secrecy. To be sure, the matter of government forcing a company to reveal its art is a serious matter. But the distribution of chemical substances into the environment requires some oversight. Especially when substances are injected into locations where they cannt be readily remediated. The remediation of an aquifer is a serious undertaking which may or may not be effective.

If you want to see what is potentially in frac fluids, go to Google Patents and search “hydraulic fracturing fluid”. A great many patents will be found. This will give the length and breadth of the compositions patented. Of this large list only a few are used in current practice. The potential carrier fluids vary from water to LPG (!). Water is a common component, but brine is said to be preferred. Additives include hydrochloric acid and surfactants. The MSDS documents may be a good source of info. Consider that a substantial threat to ground water may be that it is rendered non-potable rather than outright toxic.

Rhodochrosite Specimen with Galena and Pyrite (Copyright 2012 Th' Gaussling)

Rhodochrosite is a mineral composed of MnCO3. The specimen above is in no way exceptional, other than as a curio. The mass is comprised of rhodochrosite, galena, pyrite, what looks like quartz, and possibly a trace of a gold colored metal.

Devon Energy has raised $900 million in cash from Sinopec Group for a stake in Devon shale gas plays. These gas projects include the Utica, Niobrara, and Tuscaloosa formations.

What is interesting is not so much that China has bought its way into the extraction of a resource that the USA has in some abundance. What is more troubling is that China has bought its way up the learning curve in horizontal drilling and fracturing.

According to the article in Bloomburg Businessweek-

China National Petroleum Corp., Sinopec Group and Cnooc Ltd. are seeking to gain technology through partnerships in order to develop China’s shale reserves, estimated to be larger than those in the U.S.

“In these joint ventures, the partner does typically get some education on drilling,” Scott Hanold, a Minneapolis-based analyst for RBC Capital Markets, said today in an interview.

So, the business wizards at Devon in OKC have arranged to sell their drilling magic to the Sinopec for a short term gain on drilling activity. Way to go folks. Gas in the ground is money in the bank. These geniuses have arranged to suck non-renewable energy out of the ground as fast as possible. Once again US technology (IP, which is national treasure) is piped across the Pacific to people who will eventually use it to beat us in the market. Score another triumph for our business leaders!!

The market is like a stomach. It has no brain. It only knows that it wants MORE. Th’ Gaussling.

There is a rare earth exploration boom in progress at the present time. This boom is in response to the policy shift of the Chinese government toward greatly reduced export of crude rare earth feedstocks. This political phenomenon is the result of the grand geological lottery that has deposited mineral wealth around the world.

Billions of years ago the geological processes in play were causing the partitioning of the elements into minerals that afforded local concentrations of groups of elements. Over geological time magma rose and cooled, sequentially crystallizing out minerals that by virtue of the principles of chemistry, laid down zones of enrichment. Recrystallization, extraction, ion metathesis, hydrolysis, melting point depression, attrition, processing of melts, degassing- all processes recognizable to the chemist. These processes are responsible for the formation of mineral species as well as their transport and alteration.

But the earth is never finished processing its mineral horde. Land masses are subject to upheaval and erosion, geochemical synthesis and decomposition. Any given formation at any given time is an overprinting of frozen events separated in time.

Large zones of continent may be subject to forces that cause it to break in networks of fractures. The forces may be in the nature of shear where fracture faces slide past one another. Other forces may lead to an upthrust of rock on the continental scale leading to mountain building. The shear and bending applies forces that exceed the tensile strength of the rock, leading to fracturing. Over time these fractures may serve as channels for hydrothermal flows.

Hot, pressurized water over long periods will dissolve susceptible minerals in the rock faces and transport solutes and suspended solids throughout the fracture network. Established mineral species yield to the solvent effects of water and slough off part or all of their constituents. In doing so, the minerals are taken apart into anions and cations that will eventually reassemble elsewhere into different mineral species. Over time these fracture networks will fill with solids and self-seal. They are called veins.

Water is not innocent in its behavior. Water’s ever eager oxygen atom binds to oxophilic metals and metalloids, taking them down to the energy bargain basement of oxide or oxyanion formation. Water with dissolved acids can digest whole formations leading to cavernous voids in susceptible rock.

Over time, geological processes have left formations of elements in bodies of economically viable concentrations called ore bodies. In the case of rare earth ore bodies, these elements are found concentrated in veins and breccias, pegmatites, or dispersed at more dilute levels in many other kinds of minerals. It is a truism that the lanthanide set of the rare earths are all commonly found in the same formation, but emphasizing the lights (LREE) or heavies (HREE). Scandium and yttrium are the Group III elements grouped with the 15 lanthanides to form the rare earths. While yttrium is often found with the lanthanides, scandium is often scarce in deposits otherwise rich in the other rare earths (REE’s). It is not uncommon for REE deposits to contain significant levels of zirconium, hafnium, tantalum, niobium, thorium, and uranium.

China does not seek to deprive the world of products using REE’s. It has taken the position that the REE exports will be in the form of finished consumer products. The policy of China is that it will manage the output of rare earth-based products in a highly value added good as a means to extract the most value from it. China’s market has a central nervous system that has devised manufacturing policy. It is much like an octopus. In the US, the prevailing wisdom is that the market should seek it’s own equilibrium without government interference. Our system is a distributed in the manner of a coral reef.

Today, mining exploration firms principally from Canada, Australia, and South Africa are exploring Africa, Australia, and the Americas for deposits of REE’s- and finding them. In my survey of the field, it would seem that the US is poorly represented in the roster of rare earth exploration firms.